[ad_1]

Creator’s Observe: That is the shorter model of an article revealed on iREIT on Alpha on the thirteenth of March 2022.

Leon Neal/Getty Photographs Information

Rheinmetall AG (OTCPK:RNMBY) is likely one of the largest protection firms in Germany. It has a historical past that goes again effectively over 130 years, a market cap of round €6.6B, and it is one of many firms that has seen maybe probably the most curiosity from the current adjustments in German protection coverage.

The close to and mid-term future is prone to see important adjustments to Rheinmetall. On this article, I’ll reply crucial query of all.

Must you put money into Rheinmetall?

What’s Rheinmetall?

From the title, you would possibly assume that this firm is a few kind of metallic enterprise. This isn’t the case. Rheinmetall is a global arms producer, and it is a type of that stay in Germany after two world wars and the chilly battle.

Rheinmetall Presentation (Rheinmetall IR)

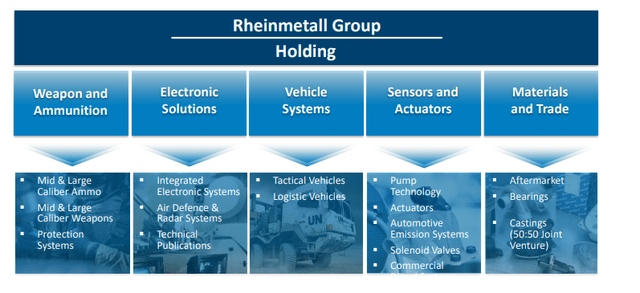

The corporate is a European play on Aerospace, automobiles, weapons, and protection. It is a protection conglomerate with 5 enterprise segments:

- Weapons & Ammunition with massive/mid-caliber weapons and their munitions, weapon stations, safety programs, powder, and so on.

- Automobile Methods, specializing in armored Bandwagons, ABC, Tower programs, Logistical Radar automobiles, Tactical automobiles, and a service sub-segment.

- Digital Options, specializing in anti-air programs, steerage programs, sensors, Cyber Safety, simulations, and so on.

- Sensors & Actuators specializing in Solenoids, Supplies, Pump Tech, Emission, and Thermo Methods and Actuators.

- Aftermarket, corresponding to Bearings, Casings, and Pistons.

The corporate would not simply construct defense-related merchandise, or it would not have survived years of low protection spending. The Rheinmetall enterprise mannequin focuses on two distinct income streams, from the segments above. The primary is the plain protection trade. The second is automotive provide components.

The protection half is especially Weapons & Ammunition, Automobile Methods, and Digital Options.

The Automotive half is present in Sensors & Actuators, in addition to the Aftermarket phase.

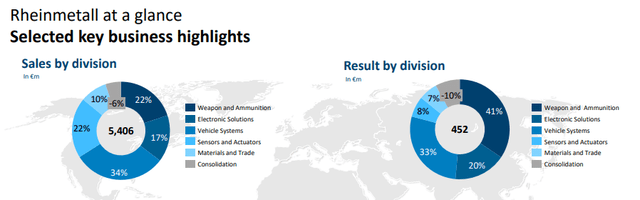

This is a extra detailed income break up of the corporate.

Rheinmetall presentation (Rheinmetall IR)

The corporate is a number one, Tier-1 automotive provider with high-tech merchandise throughout the ICE, EV and FC worth chain, with elements and subsystems for hydrogen know-how as effectively.

This income break up signifies that basically talking, Rheinmetall is in an excellent place to essentially make the most of the elevated geopolitical instability we’re seeing right here. With different segments seeing tailwinds on account of ESG, EV, and inexperienced tech in addition to hydrogen, the corporate is in a great place to essentially see its revenues enhance transferring ahead.

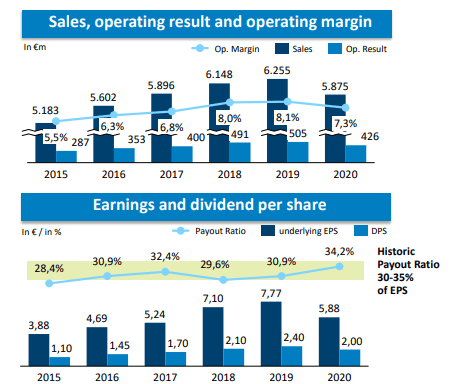

Rheinmetall is successful story within the context of a 10-year development, on account of profitable portfolio strikes, together with divestments, reorganizations, resulting in elevated gross sales, margins, and outcomes.

Rheinmetall Presentation (Rheinmetall IR)

The corporate can be a surprisingly ready and secure dividend payor, with not even COVID-19 making that a lot of a dent within the dividend report. The corporate has no credit standing price mentioning, but in addition has zero debt. It has a web debt/EBITDA of -0.02X as of 2021E.

Rheinmetall was in a foul spot about 9-10 years in the past, however because of the aforementioned restructuring had been capable of save its enterprise, margins, and core areas. This isn’t to say that the corporate is worry-free. Margins within the Electronics options/Protection segments proceed to be beneath par on account of some points out of Norway and Brazil, although it is seemingly we’ll now see a turnaround right here.

The explanation for the margin and operational slippage in 2013-2014 was considerably reduce protection spending in Europe.

That’s now, clearly, fully reversed.

The automotive phase in the meantime, is chugging alongside very properly, with strong divisional margins on account of transferring its manufacturing base to low-cost international locations corresponding to Mexico, China, and India, with robust development for mechatronics and hardparts for each segments. The margin right here is approaching double digits.

Nevertheless, the corporate has been focusing on a discount in automotive to cut back the volatility. The corporate additionally targets a below-20% ICE publicity over time, with 70% 2025E gross sales to the protection sector, and 10-15% in the direction of the EV sector.

Rheinmetall Presentation (Rheinmetall IR)

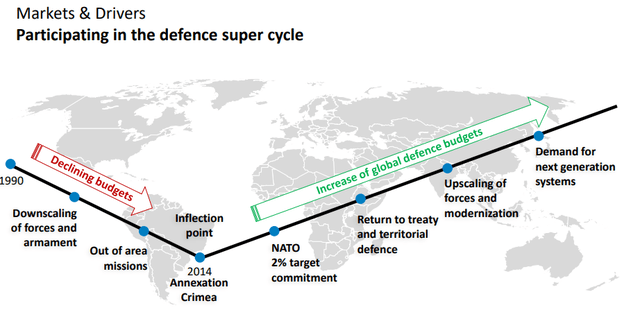

So Rheinmetall’s goal is to develop into primarily a protection play, with a minor deal with EV and automotive/ICE purposes over time. Given current occasions, it appears extra seemingly that the corporate would possibly be capable to handle this. There are additionally clear market drivers for such a growth, together with tightening rules, elevated demand for protection budgets, connectivity and digitization of armed forces, modernization of present belongings and new options for previous merchandise – corresponding to hybrid/hydrogen.

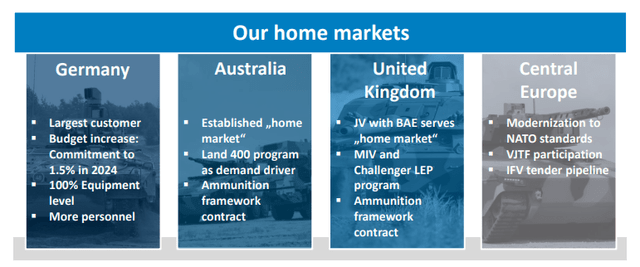

For this reason the corporate targets gross sales of €8.5B in 2025E, with a ten% RoE goal and a CF/Gross sales ratio of three.5%. Protection spending has additionally been a protected, anti-COVID guess, with budgets rising and tenders persevering with regardless of the pandemic. The corporate’s markets, together with Australia, UK, Germany, Hungary and USA are all rising. A number of of those are thought-about to be Rheinmetall’s “House” markets.

Rheinmetall Presentation (Rheinmetall IR)

The corporate expects the German protection price range to extend massively over the subsequent few years, rising 45% since 2014. The corporate’s portion of that price range is sort of 35% within the nation, making Rheinmetall a vital play on German protection, in the identical means, that Thales (OTCPK:THLLY) is a proxy to the French protection price range.

Greater than 46% of the corporate’s revenues is a pure protection play with interesting margins which are allowed for a wholesome kind of development and is prone to proceed offering wonderful development transferring ahead. The corporate can be an lively M&A’er when wanted, with the final M&A being Gemalto. Rheinmetall has a really robust R&D focus and is on the forefront of cyber safety.

As well as, and as I discussed earlier than, the corporate has most likely the strongest stability sheet on your entire German protection market, and this may solely develop stronger as its margins and money circulate technology are improved much more because the protection supercycle intensifies.

The necessity to digitize nearly each present land system within the German military alone is a contract price over €10B – and that is solely the start for Rheinmetall. This was, by the best way, already within the pipeline previous to the battle – it is solely develop into extra necessary now.

New markets are additionally fascinating for the corporate, and Rheinmetall is growing JVs with BAE Methods (OTCPK:BAESY) with a purpose to create a “new” dwelling market within the UK, and there are many potential procurements which now in fact are trying higher and higher as a result of battle.

Rheinmetall Presentation (Rheinmetall IR)

General, I deem that Rheinmetall is strictly what it looks as if. It is a conservative German participant in Aerospace/Protection that even previous to this battle was in an excellent place for the subsequent few years. It was a “BUY”, albeit with a decrease upside, even at the moment, and I used to be taking a look at it favorably.

What this battle did is in fact dial that upside as much as maybe twice as excessive.

I’ve by no means been a fan of shopping for a enterprise on account of traits. If this firm wasn’t enticing previous to the battle, I would not put my chips down on it now both – however the battle has solely made this firm’s upside even higher, and that is why I am viewing it favorably right here.

The European protection sector is an enormous place, with not less than 7-9 varied friends that deserve point out in their very own proper. I intend to cowl these companies successfully, and I’ve already lined Airbus (OTCPK:EADSY). Evidently, I pushed extra money into Airbus as effectively, and I am at the moment reviewing the entire firms on this phase to see the place the strongest prospects are.

Rheinmetall, being 30%+ of the German protection price range, is certainly one of many highest on that checklist.

Rheinmetall – The dangers

Naturally, no firm is with out danger. Neither is that this one. The corporate’s continued publicity to automotive is not essentially a foul one. Nevertheless, it does include a 20% Diesel drag, which is prone to stay for so long as the corporate is within the sector. Whereas restructuring has been profitable, the margins in these segments are decrease, and their demand cycle could be much more unstable than the corporate’s different operations.

Moreover, the corporate has been making an attempt to develop extra on a global foundation – a great factor, but in addition comes with elevated competitors, in addition to FX danger.

Whereas Rheinmetall is critical in Germany, it stays a small participant in comparison with a few of its friends – and most actually to a few of the bigger US firms on this sector.

Maybe most significantly are the authorized dangers to investing in protection in Germany, on account of extremely restrictive export insurance policies. The German authorities is extraordinarily stringent about these items.

German navy tools exports are ruled by the Primary Regulation (Grundgesetz – GG), the Battle Weapons Management Act (Gesetz über die Kontrolle von Kriegswaffen – KWKG), and the Overseas Commerce and Funds Act (Außenwirtschaftsgesetz – AWG) along side the German Overseas Commerce and Funds Regulation (Außenwirtschaftsverordnung – AWV). The “Political Rules Adopted by the Authorities of the Federal Republic of Germany for the Export of Battle Weapons and Different Army Gear” of 19 January 2000 and the Council Frequent Place of the EU defining widespread guidelines governing management of exports of navy know-how and tools of 8 December 2008 present the licensing authorities with pointers.

With regard to protection tools, the Federal Republic of Germany distinguishes between battle weapons and different varieties of navy tools. Virtually all export licenses for navy tools are granted for EU international locations whereas the availability of navy tools to international locations in which there’s an arms embargo (by the UN, EU, or OSCE) is nearly unattainable. For different international locations, the German authorities will decide on a case-by-case foundation, paying specific consideration to the factors set out within the EU Code of Conduct.

What this implies, and the way I might interpret this, is that any growth exterior of the EU is prone to be problematic, placing a theoretical cap on Rheinmetall that is not present in all different protection firms.

Rheinmetall’s valuation

Nevertheless, no danger can take away the potential upside we’re seeing right here. The EU appears set on arming itself, so protection firms are one thing we should be taking a look at right here. Resulting from a current, large valuation explosion in Rheinmetall which we additionally noticed in most protection firms, the fundamentals-based valuation targets are all comparatively tepid. What I imply by that is that the present upside for Rheinmetall is extraordinarily tilted in the direction of future development estimates.

From a DCF perspective, I am assuming that Germany follows via with its 2% of GDP, which might be a doubling of the earlier ones, and it’ll then rise to above 2% of the GDP. It is also the truth that the working margin for this enterprise is extraordinarily favorable.

On the again of this, I am assuming a development fee in EBITDA of 6-8% and gross sales development of 4-6% for the approaching 3-5 years. I am additionally assuming a 3% CapEx/gross sales development, which is in keeping with the historicals. A WACC of 9.15% brings this DCF to an implied EV/share of between €220-€270. That is an especially big selection – however then the sensitivities and assumptions are extraordinarily excessive.

Additionally, as I stated, and actually keep in mind this, that valuation is predicated on the very fact, virtually solely, of that protection spending development.

So as views, we see extra of a “mellow” growth. Public comps embrace Thales, Leonardo (OTCPK:FINMY), Valeo (OTCPK:VLEEY), BAE Methods, and others. The typical valuation for these firms ranges between 5-18X P/E (a large unfold), with a median of round 11X. That makes Rheinmetall overvalued right here, not simply on P/E, however on EV/EBITDA and on ebook values. The typical yield within the phase is round 3%, which once more makes Rheinmetall considerably overvalued with its present 2.1% yield as a result of large valuation spike we have been seeing.

In the case of NAV/SOTP, I am assigning a better, 10-14X EV/EBIT a number of to the corporate’s protection phase, trending in the direction of 14X given the current focus right here, and a considerably decrease 7-9X EV/EBIT as a result of automotive margin weak spot (comparatively). The corporate has no different important belongings, coming to a complete of round €8.7-€9.5B gross, and round €7.6-€8.4B web, with a share depend web of the treasury of round 43.2M. This means a NAV/share of round €175-€194/share, implying an undervaluation right here.

The right way to weigh and premiumize Rheinmetall right here is tough. It is a legacy participant, a proxy to the German protection price range, nevertheless it’s additionally overvalued right here in keeping with something besides a SOTP or a high-growth DCF valuation.

S&P World provides us some ideas right here. 11 analysts vary between averages of €83 and €205 – a large variance coming to a median of about €148, with 8 out of 11 at the moment contemplating Rheinmetall a “BUY”. Whereas these are ideas, a variety corresponding to this actually provides us little or no assist.

What I say is that this.

Rheinmetall’s attraction largely relies on how deeply impacted you imagine that the EU and the rest of the world – however largely Germany – shall be for the subsequent few years.

Should you imagine that Germany will follow and possibly even enhance its plans right here, then this is not only a good firm, it is an excellent play total. The extra constructive you are on this, the upper you’ll be able to weigh the DCF/Progress-related estimates, and permit for basic premiums for Rheinmetall.

I would watch out letting this get out of hand although. For myself, I am electing to weigh DCF lower than 25%, however I’m assigning the corporate a ten% premium to mirror the titanium-like place on the German protection market. When weighing the totally different views like that, I find yourself round €155-€172 – considerably decrease than the DCF, however nonetheless at a possible upside on the upper vary.

Fairness analysts Alpha Worth maintain a €210/share worth goal for the corporate – one which I imagine far too closely assumes the DCF development state of affairs to materialize. At such valuations, not even substantial DGR would supply a great yield. I see how they get there – however I select to take a extra conservative route.

I am at all times cautious on the subject of this kind of momentum. The corporate – as most protection companies – have seen a large kind of valuation development, which I view as long-term debatable. We have already seen some drop-off right here.

And whereas I staked out my preliminary place (only a few shares) the day after Putin invaded Ukraine, I am hesitant to go all-out on Rheinmetall simply but – after not doing so initially.

Nevertheless, I select to take the mid-point of my steerage, coming to round €164/share, as my PT for the enterprise.

And on this foundation, Rheinmetall is a “BUY”.

Thesis

Tempers are heated, and with scorching tempers come a scorching inventory market. Just like the “nutty” valuations for work-from-home firms we noticed throughout COVID-19, we’re now seeing a large circulate into protection shares on account of geopolitical tensions.

I would be the first one to remind you that a lot of this premium could be unwound in a comparatively quick time if issues change.

Nevertheless, I’ll state to you, expensive readers, that we’re seeing a basic change within the protection insurance policies of the European Union.

So a few of these premiums and excessive valuations are very a lot justified. And I do imagine Rheinmetall is up there.

The corporate’s ADR is comparatively thinly traded, correlated to its smaller market cap. RNMBY is a 0.2X ADR, and I would not actually inform anybody to purchase this, however somewhat deal with making an attempt to get entry to the natively-listed German share. I might argue that in the long term, Rheinmetall has a possible RoR upside of between 8-12% yearly, or a direct upside to its valuation of round 8% – although observe that many analysts take into account the upside to be far larger than this, and Alpha Worth considers it to be over 30%.

If we do see a large kind of gross sales spike, it isn’t unlikely that Rheinmetall gross sales numbers may climb in the direction of €9-€10B within the coming years, which in flip would assist dividends of upward of €5-€6/share, if the present remuneration coverage was to proceed to be adopted.

General, I like Rheinmetall right here – however I am additionally conscious that there is appreciable emotion concerned, the place I sometimes wish to put money into “disliked” firms after they’re extraordinarily low cost.

[ad_2]

Source link

{kind=link}